TL;DR:

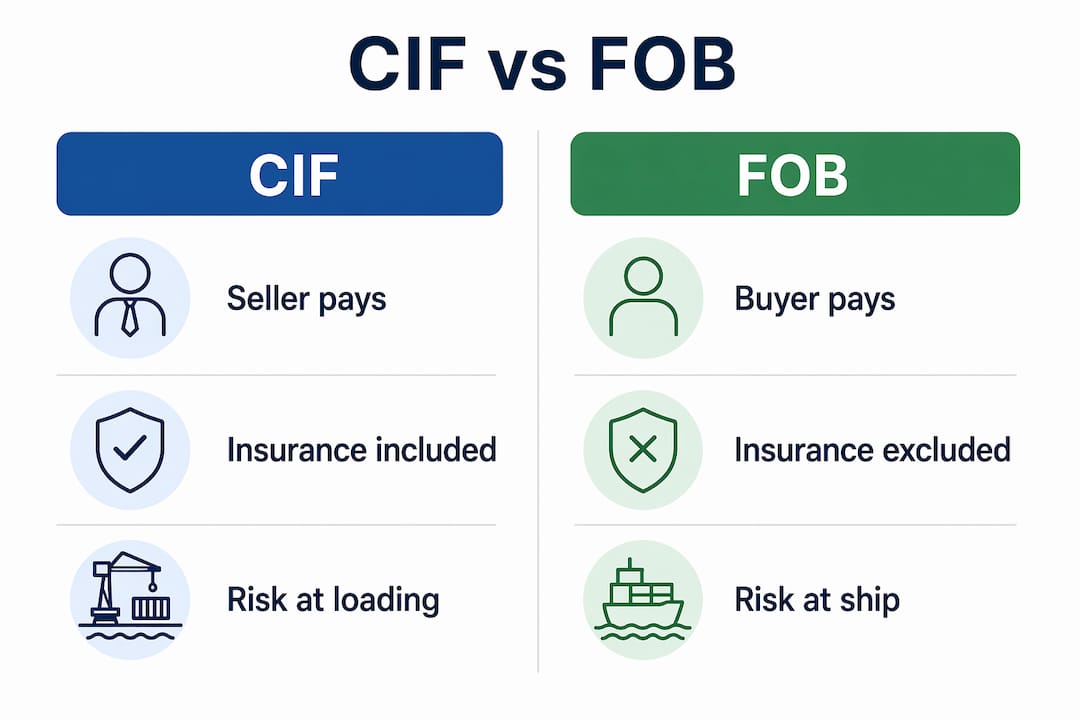

- CIF requires the seller to pay costs and insurance until the vessel’s destination port, but risk transfers at loading. Buyers assume risk immediately once goods are onboard, even though the seller continues paying for ocean freight and minimum insurance. The standard CIF insurance coverage often excludes common risks like theft and water damage, which can leave buyers unprotected.

Cost Insurance Freight (CIF) is defined as an Incoterm under which the seller pays for the goods, ocean freight, and minimum cargo insurance to a named destination port, while the buyer assumes risk the moment goods are loaded onto the vessel. Governed by the International Chamber of Commerce (ICC) Incoterms 2020 rules, CIF is one of the most widely used terms in bulk maritime trade. The cost insurance freight meaning trips up importers and exporters alike because it splits cost responsibility and risk responsibility at two different points in the journey. Understanding exactly where each obligation starts and stops protects your cargo, your budget, and your legal position.

What does cost insurance freight mean for sellers and buyers?

CIF assigns the seller a clear set of financial obligations that extend all the way to the destination port. The seller covers export clearance, main carriage freight, and minimum cargo insurance, while the buyer takes over once the goods arrive. That handoff point sounds simple, but the cost split has real consequences for how you price goods and structure contracts.

The table below maps each stage of the shipping process to the responsible party under CIF terms.

| Shipping stage | Seller’s responsibility | Buyer’s responsibility |

|---|---|---|

| Export packaging and labeling | Yes | No |

| Export customs clearance | Yes | No |

| Loading onto vessel at origin port | Yes | No |

| Ocean freight to destination port | Yes | No |

| Minimum cargo insurance (ICC©) | Yes | No |

| Import customs duties and taxes | No | Yes |

| Unloading at destination port | No | Yes |

| Inland delivery to final destination | No | Yes |

The delivered price a buyer pays under CIF already includes the cost of goods, the ocean freight rate, and the insurance premium. That bundled price can look attractive because it removes the need to arrange freight separately. The catch is that the buyer has limited control over which carrier or insurer the seller selects, and the minimum insurance standard is often lower than buyers expect.

Pro Tip: Always request a copy of the freight contract and insurance certificate before the vessel departs. Sellers are required to provide these documents under Incoterms 2020, and reviewing them early lets you spot coverage gaps before a claim becomes necessary.

How does risk transfer under CIF work?

Risk transfer under CIF happens at a specific moment: risk passes to the buyer as soon as the goods are loaded onboard the vessel at the port of shipment. This surprises many importers who assume the seller carries risk until the goods arrive at the destination port.

The seller pays freight and insurance costs for the entire ocean leg, but those payments do not extend the seller’s risk exposure. If a storm damages the cargo mid-ocean, the buyer bears the financial loss, even though the seller arranged and paid for the insurance policy. The buyer must file the claim directly with the insurer using the documentation the seller provides.

Risks the buyer assumes from the moment of vessel loading include:

- Loss or damage caused by rough seas or weather events

- Theft or pilferage during ocean transit

- Contamination from adjacent cargo

- Delay-related losses not covered by the insurance policy

- General average contributions if the vessel declares an emergency

This split between cost payment and risk ownership is the defining feature of CIF. It is also the feature most likely to create disputes when something goes wrong. Buyers who do not review the insurance certificate before shipment often discover the coverage excludes the exact type of loss they suffered.

Pro Tip: If your cargo is containerized or high-value, negotiate ICC(A) all-risks coverage in the sales contract before the seller books the shipment. Changing the insurance level after loading is not possible.

What level of insurance does CIF actually provide?

The minimum insurance coverage under CIF is Institute Cargo Clauses ©, a named-perils policy that covers only major catastrophic events such as vessel sinking, stranding, fire, or explosion. ICC© does not cover the transit risks most commonly experienced in practice.

Specifically, ICC© excludes theft, pilferage, contamination, damage from rough handling, and water damage. These are among the most frequent causes of cargo loss in international shipping. A buyer receiving electronics, pharmaceuticals, or consumer goods under a standard CIF contract with ICC© coverage carries significant uninsured exposure.

The table below compares the two main insurance levels relevant to CIF and CIP shipments.

| Feature | CIF insurance: ICC© | CIP insurance: ICC(A) |

|---|---|---|

| Coverage type | Named perils only | All risks (with standard exclusions) |

| Theft and pilferage | Not covered | Covered |

| Water damage | Not covered | Covered |

| Breakage and rough handling | Not covered | Covered |

| Typical cargo suitability | Bulk commodities | Containerized and high-value goods |

| Incoterms 2020 default | CIF minimum | CIP minimum |

The 2020 Incoterms revision deliberately kept CIF insurance at ICC© to suit bulk maritime trade, while CIP was raised to the more comprehensive ICC(A) standard to reflect the wider risk profile of containerized cargo. That policy decision means CIF is well matched to bulk grain, coal, or ore shipments, but poorly matched to manufactured goods shipped in containers.

Carrier liability under international conventions like the Hague-Visby Rules is limited to SDR amounts far below commercial value. Buyers should never treat carrier liability as a substitute for cargo insurance. Reviewing the seller’s insurance certificate and understanding its exclusions is the only way to know whether your cargo is adequately protected. For a deeper look at coverage options, the freight insurance guide from Worldwideexpress covers the full range of policy types available to international shippers.

Pro Tip: Insert a clause in your purchase contract requiring the seller to provide ICC(A) coverage. Sellers often agree to this at minimal additional cost, and it eliminates the most common coverage gaps before the shipment moves.

How does CIF compare to FOB, CFR, and CIP?

CIF sits within a family of Incoterms that share some features but differ in critical ways on cost, insurance, and risk. Understanding those differences helps you choose the right term for each trade relationship.

CIF vs. FOB. Under Free On Board (FOB), the buyer arranges and pays for both freight and insurance from the port of origin. Risk transfers at the same point as CIF: when goods are loaded on the vessel. The practical difference is that FOB gives the buyer full control over carrier selection and insurance coverage. CIF hands that control to the seller, which can be convenient but limits the buyer’s ability to manage cost and coverage quality.

CIF vs. CFR. Cost and Freight (CFR) mirrors CIF exactly except it removes the seller’s insurance obligation. The seller pays freight to the destination port, risk transfers at loading, and the buyer must arrange their own insurance. CFR is useful when the buyer has a preferred insurer or wants to consolidate insurance across multiple shipments under a single open cover policy.

CIF vs. CIP. Carriage and Insurance Paid To (CIP) is the multimodal equivalent of CIF. It applies to any mode of transport, not just ocean freight. CIP requires ICC(A) all-risks coverage rather than the ICC© minimum. Risk under CIP transfers when goods are handed to the first carrier, not at vessel loading. CIP is the better choice for containerized cargo moving door-to-door.

Practical scenarios where CIF is the right choice:

- Bulk commodity trades such as grain, fertilizer, or coal where ICC© coverage matches the risk profile

- Transactions where the seller has established freight contracts offering better rates than the buyer could negotiate independently

- Markets where the buyer lacks local freight forwarding relationships at the origin port

Scenarios where CIF is less suitable:

- Containerized shipments of electronics, pharmaceuticals, or fragile goods requiring all-risks coverage

- Trades where the buyer wants full control over carrier selection and insurance terms

- Multimodal shipments involving road or rail legs before ocean loading

Key Takeaways

CIF places cost responsibility on the seller through the destination port but transfers risk to the buyer at the moment of vessel loading, making insurance quality the single most important variable in any CIF contract.

| Point | Details |

|---|---|

| Risk transfers at loading | The buyer bears loss or damage from the moment goods are onboard the vessel, not at destination. |

| ICC© is the minimum standard | CIF insurance covers only named catastrophic perils and excludes theft, pilferage, and water damage. |

| Sellers must provide documents | The commercial invoice, bill of lading, and insurance certificate must be tendered to trigger buyer payment. |

| CIF suits bulk cargo best | Containerized or high-value goods need ICC(A) coverage negotiated into the sales contract. |

| Carrier liability is insufficient | Hague-Visby limits fall far below commercial cargo value, making cargo insurance non-negotiable. |

The gap most CIF users never see coming

The single biggest mistake I see traders make with CIF is treating the insurance certificate as a formality. They receive it, file it, and never read it. Then something goes wrong mid-ocean and they discover their ICC© policy excludes the exact cause of loss.

Bulk commodity traders have used CIF for decades with good reason. The ICC© minimum matches their risk profile well. A vessel sinking or a fire is the catastrophic event they need covered, and ICC© delivers that. But the moment you put electronics, textiles, or food products in a container under a standard CIF contract, you are carrying risks the policy was never designed to cover.

The risk transfer timing is the other issue that catches importers off guard. You own the risk from vessel loading, but you do not control the vessel, the route, or the carrier’s handling practices. If the ship is rerouted through a storm zone and your cargo is damaged, the claim is yours to file, using the insurer the seller chose, under the policy terms the seller negotiated. That is a significant loss of control for the party carrying the financial exposure.

My advice is straightforward. Negotiate insurance level and carrier approval rights into every CIF contract before signing. Require ICC(A) for anything other than bulk commodities. Request the insurance certificate and bill of lading before the vessel departs so you can verify coverage while there is still time to act. And understand that filing a cargo claim under a policy you did not select requires careful documentation from day one.

— Ian

How Worldwideexpress supports your CIF shipments

Navigating CIF terms requires more than knowing the definition. It requires verifying insurance certificates, confirming documentation is complete before a vessel departs, and knowing exactly when your risk exposure begins.

Worldwideexpress specializes in international logistics services that cover every stage of a CIF shipment, from export documentation review to import customs clearance and cargo insurance verification. The team works with importers and exporters to confirm that insurance coverage matches cargo type, that sellers have tendered the required documents, and that risk transfer timing is clearly understood before goods leave the origin port. Whether you are importing bulk commodities or containerized goods, Worldwideexpress provides the freight expertise and documentation support to keep your shipments protected. Get a freight quote or speak with a logistics specialist to review your current CIF terms.

FAQ

What is the cost insurance freight meaning in simple terms?

CIF is a shipping term where the seller pays for the goods, ocean freight, and minimum cargo insurance to a named destination port. The buyer assumes risk as soon as goods are loaded onto the vessel at the origin port.

When does risk transfer to the buyer under CIF?

Risk transfers to the buyer the moment goods are loaded onboard the vessel at the port of shipment, even though the seller continues to pay freight and insurance costs for the ocean leg.

What insurance coverage does CIF include?

CIF requires the seller to provide Institute Cargo Clauses © coverage, a named-perils policy that excludes common risks like theft, pilferage, water damage, and breakage. Buyers can negotiate ICC(A) all-risks coverage through the sales contract.

What is the difference between CIF and FOB?

Under FOB, the buyer arranges and pays for freight and insurance from the origin port. Under CIF, the seller arranges and pays for both, but risk still transfers at vessel loading under both terms.

Does CIF cover inland delivery at the destination?

CIF does not cover inland delivery. The buyer is responsible for unloading at the destination port, import customs clearance, duties, and all inland transportation to the final destination.

Recommended

- Freight Insurance for International Shipments: 2026 Guide – Worldwide Express, Inc.

- 7 Smart Freight Insurance Options for Safer Shipments – Worldwide Express, Inc.

- 8 Key Freight Terms Definitions Every Importer Should Know – Worldwide Express, Inc.

- Freight contract terms: essential guide for shipping managers – Worldwide Express, Inc.